Facebook

Facebook  Twitter

Twitter  Soundcloud

Soundcloud  Youtube

Youtube  Rss

Rss

Chemin de Fer sur l’├пle de Khone

In recent weeks, the Lao Government approved the idea of borrowing a reported amount of USD 7.2 billion to fund construction of a 418km passenger and freight railway connecting Vientiane to Yunnan province, China.

Despite a number of articles and announcements about this rail project, there remains a lack of detailed discussion about the economic implications for Lao.

The most detailed information available about the project comes from a report delivered by the Vice Prime Minister and advisor on economic development of Lao, Mr. Somsavath Lengsavath, to the National Assembly on 18 August 2012. In the report, the railway is justified to transform Lao from a land-locked nation to a land and sea-linked nation. The growth of China and ASEAN-China trade links are central arguments used to justify the project. The report discusses a feasibility study that demonstrated a financial internal rate of return of 4.56 percent and an economic internal rate of return of 32.97 percent.

Yet despite the Government’s enthusiasm, The Asian Development Bank has said the project is “unaffordable” and the World Bank has said “A careful review of the implications for debt sustainability, in addition to careful cost-benefit analysis, is … critical before proceeding.”.

Looking at the numbers involved provides some insight into why this project is a big cause for concern. Especially when Lao is already considered by the IMF to be at high risk of debt distress and has taken on a “large amount of undisbursed loan commitments from China”.

The most commonly discussed measure of the potential scale of the loan is the size of the loan compared to Lao’s GDP. This figures is given as about 87 percent. The aforementioned report on the project suggests a proposed loan principal of RMB 37.9 billion with interest of RMB 6.1 billion. Converted to USD, these figures combined come to approximately 7.2 billion, the figure that is commonly discussed for the project. In most articles, this has appeared as the principal, with interested calculated on top. Based on the report of the Vice Prime Minister, it would appear that the actual proposed principal amount is actually closer to USD 6.15 billion, approximately 74 percent of Lao’s GDP in 2011.

Lao already has an estimated debt of $5.95 billion, meaning total debt-to-gdp would potentially rise to 146 percent. This would make Lao the fourth most indebted country in the world after Japan, Zimbabwe and Greece.

Such ratios should not to be ignored, but the real determinant of fiscal stability is the willingness of creditors to extend loans and the ability for Lao to repay its debt.

China and specifically, the China EXIM Bank is being discussed as the likely source of funds. The China EXIM Bank had stated assets in 2011 of RMB 1,199 billion. A loan of RMB 37.9 billion would equate to 3 percent of the EXIM Bank’s total loan book. This is not an insignificant amount, especially since the capital amount proposed by Lao is likely to be an underestimate due to several costs being excluded from calculations. Namely, the costs for compensation of land, removal of unexploded ordinance, security of the construction team, the potential use of liquid fuel where electricity from hydropower isn’t available and a contingency for unforeseen cost increases.

Even with strong support from Beijing for this project, the EXIM Bank will need to scrutinise this project and the final terms may not be as generous as currently proposed by the Government of Lao.

In-fact, a recent report through Radio Free Asia suggests that the EXIM Bank may not be willing to extend such favorable terms and an interest rate of 5.8 percent has been mentioned, rather than 2 percent.

Unfortunately, final details of the amount and terms of the loan are yet available. The report on the project by the Vice Prime Minister suggests that Lao is continuing to work with the Chinese on this and will release further details as part of a ‘debt contract’.

Whatever the final terms are, there are three basic ways for Lao to repay the loan. Through the annual budget with money generated primarily from mineral royalties and taxation. Through the income generated from the rail project itself and via guarantees on mineral resources.

The fact that the original Chinese partner pulled out of the project because it was deemed to be unprofitable indicates that the ability of the railway to pay for itself is unlikely. In-fact, very little information is available about the estimated ongoing operating and maintenance costs and it is possible that further loans or spending could be required if the project is unprofitable and requires further capital from the central government. As for the construction and early year costs being discussed at the moment, it is likely that Lao will fund the construction of the project through the budget and/or mineral resources.

The impact of principal and interest repayments of this size on the national budget will be significant and likely to cut into existing services. Additionally, because the loan is denominated in RMB, potential exchange rate fluctuations between the Lao KIP and the RMB will impact on annual repayments. Because the central bank of Lao pursues a ‘managed floating exchange rate regime’ significant changes could have ramifications for Lao’s foreign exchange reserves.

In 2010/11, the Government of Lao reported revenue (including foreign grants) of USD 1.8 billion and expenditure of nearly USD 2 billion, but reported a deficit of USD 0.6 billion, 75 percent of which is financed through foreign grants. Expenditure by the government can be divided roughly in half to either ‘current expenditure’ or ‘infrastructure’.

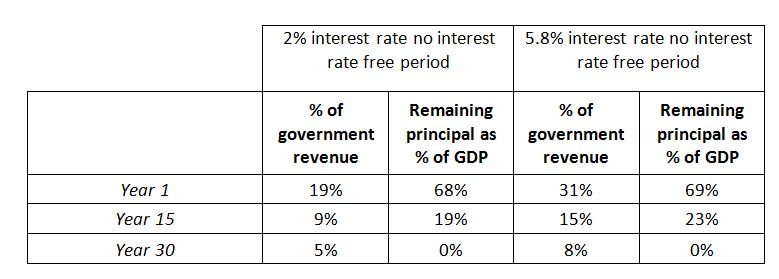

Assuming no 10-year interest free window but a favorable 2 percent interest rate, principal and interest payments for the proposed railway loan would take up 19 percent of government revenue at the end of year 1. This would have to come from cuts to current expenditure or existing infrastructure. If the interest rate were to rise to the reported 5.8 percent, this percentage would increase to 31 percent.

(Click table for larger image)

In other words, the principal and interest payments will potentially take up a significant chunk of government revenue, particularly in the first 5 to 10 years, and will always be a very noticeable item on the budget. And these are all highly dependent on forecast growth in GDP and government revenue as well as any additional costs of the project.

Because the loan is likely to be denominated in RMB, an additional major concern is the potential for exchange rate fluctuation and the impacts of this on debt serviceability.

Should the RMB increase in value against the KIP by just 10 percent, the debt burden would increase accordingly. In other words, a RMB 37.9 billion loan could become a RMB 41.7 billion loan in a short amount of time. If in such a year mineral prices or output were also at cyclical lows, the ability of Lao to service the debt could be impacted, since mining accounts for a large chunk of government revenue and export (and so forex) earnings)

If Lao over-borrows, there are several implications for various stakeholders.

Firstly, Lao will experience lower growth and austerity for a long time as government revenue effectively subsidises a loss-making project.

Second, Lao will need to accumulate significant quantities of RMB in order to service the loan. The actual mechanisms for this are difficult to predict but is likely to be the reason for using mineral resources as collateral. The implication for Laos is that it will end up locking itself into a single buyer, which may result in lower than world prices for minerals.

Thirdly, financial restraints may ensue as Lao is seen as a risky place to lend and as debt is written down, causing losses to banks and potentially depositors. This may also result in currency depreciation which would further strain Lao’s ability to service debt denominated in foreign currencies.

And finally, that a debt restructuring will take place in which Lao negotiates with its creditors to alter the timing, duration of debt and the interest rate paid.

Given Lao’s dependence on mineral resources and the proposed guarantee for the loan from such resources, the impacts of fiscal mismanagement could also impact the minerals sector.

The outcomes above are not a foregone conclusion, but they point to the scenarios that may play out if Lao borrows for a project that fails to deliver sufficient returns commensurate to the costs and risks involved.

These benefits can be conservatively estimated at USD 275 million annually. That is, the project needs to direct (profits) or indirect (GDP and consequent government revenue growth) of at least USD 275 million per year to pay its way. But this only considers the capital costs for construction and early year costs and doesn’t factor in cost blowouts or the potential for operating losses. So in reality, this figure may be much higher.

Based on the reported benefits listed in the 2012 report by the Vice Prime Minister, we can hazard a simplistic preliminary benefit-cost analysis. The results of this are outlined in the table below.

(Click table for larger image.)

As the figures in the table show, the profits from the project are unlikely to cover the cost of the project. The key direct benefit is estimated to arise from benefits to customers in the form of reduced time for transportation, volume of transportation and improved service quality. Somewhat surprisingly, it is suggested that the key indirect benefit will come through digging and developing ‘new sources of natural resources’. It is unclear how these benefits were calculated. Further, no direct and indirect non-financial costs have been included, overstating the net benefits.

Nonetheless, taking these figures at face value, we can estimate a simple benefit-cost ratio (BCR) of 0.76 based on profits generated as a proportion of costs of the project. A direct economic BCR is estimated at 3.75 and total economic BCR at 9.55.

Due to the inclusion of benefits without sufficient transparency regarding assumptions and methodology and the lack of direct and indirect economic costs, these figures are overstated, potentially by a significant magnitude.

The economic, social, environmental and political repercussions of the proposed Vientiane to Yunnan railway will be felt for a generation. A rigorous and transparent benefit-cost analysis including detailed plans for servicing of construction debt as well as a business plan and forecast operational cash flows should be made available to assess the merits of the project. Details of wider economic costs and benefits should also be made available, along with the assumptions that underpin any estimates.

Stakeholders inside and outside Lao should be demanding this information now, before it is too late.

Tristan Knowles is a Director of Economists at Large.