Facebook

Facebook  Twitter

Twitter  Soundcloud

Soundcloud  Youtube

Youtube  Rss

Rss

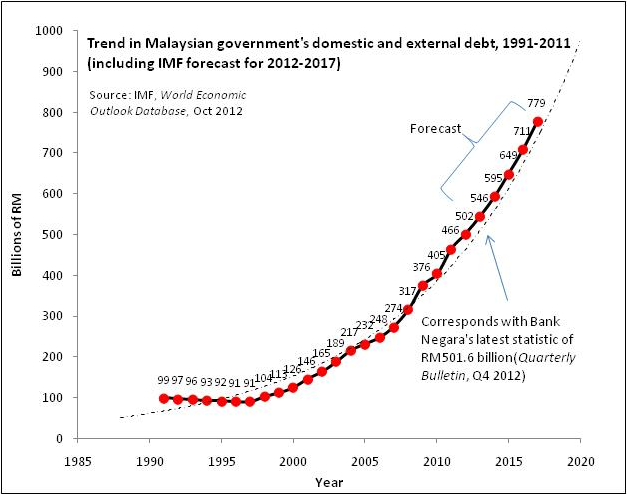

Malaysia came out of the ‘Great Recession’ relatively little the worse for wear, but bearing a higher burden of debt than is common among emerging markets, both in the public as well as in the private sector. While concern over Malaysia’s public sector debt has been less evident in the public discourse lately, those concerns are never far away. At 52.9% of GDP in 2012, the debt level is nowhere near the onerous burdens carried by many advanced economies, with much of the increase in debt due to the 6.7% fiscal deficit incurred during the Great Recession.

Yet public sector debt remains far above the regional average and while not in itself dangerous, it does limit the ability of the government to counteract future crises. Arguments against the government’s debt level are thus now framed in terms of improving “fiscal space”. For example, in the latest Article IV Consultation, this is what the IMF had to say:

Malaysia’s fiscal space has shrunk considerably following the global financial crisis…A weak structural fiscal position and a relatively high debt ratio reduce the ability to mount countercyclical fiscal responses in the future.

There are quite valid concerns over the sustainability of government revenue and expenditure. The tax base is narrow with less than 10% of the workforce actually paying taxes, while a third of government revenue comes from taxes and dividends on the oil & gas industry, which over the long term is threatened by potentially declining reserves and more recently, lower global prices. Nevertheless, the overall debt to GDP ratio is below any critical threshold, and the government carries minimal external debt with over 95% raised domestically. The financial system has more than sufficient excess liquidity to absorb further debt issuance, and both interest rates across the term structure and debt service ratios are at near all time lows.

So while immediate concerns over a Malaysian sovereign debt crisis are substantially overblown, the case for reducing the debt to GDP ratio makes sense. This is especially true since the economy appears to be growing along its potential-output growth path which means, whether viewed from the lens of neo-classical or Keynesian macroeconomic thought, fiscal consolidation in Malaysia is thus both necessary and appropriate.

The question remains as to how to go about it. Much of the government’s financial commitments are “sticky” – salaries, pensions and debt service payments make up nearly 40% of the 2013 Budget. The development budget (which is fully funded through debt) is discretionary, but cuts here would reduce future potential growth, and limit investment in needed infrastructure. The two other major items of expenditure that could be ripe for the plucking are procurements and subsidies, which combined total nearly 30% of total government expenditure.

Shifting to a largely open-tender based procurement approach, as the government has committed to doing, could yield some savings by plugging leakages and wastage. But gains here may be more limited than one might imagine – open tenders may be more cost-effective in theory, but much of these efficiency gains are lost as procurement needs grow larger and more complex.

Subsidy reduction offers greater scope for cost savings. The federal government expects to spend RM37.6 billion (about US$12.3 billion) on subsidies in 2013, of which the largest portion will go towards maintaining below market petrol and diesel prices. In addition, there is the “hidden” subsidy borne by the national oil company Petronas, which provides natural gas below market prices to domestic power producers, industry, and consumers. In 2011, this subsidy amounted to an additional RM18.7 billion (US$6.1 billion).

Rationalising subsidies would go a long way towards reducing the deficit, and begin making a dent in reducing the government’s debt load. While this has met with considerable and understandable civil and political opposition, there’s no doubt that any future administration will need to address this issue. The long overdue implementation of GST would also, on the revenue side, help close the fiscal gap.

But leaving aside the effort to improve fiscal space, of more pressing concern is Malaysia’s private sector debt, specifically household debt. Malaysian corporate gearing ratios have been generally declining since the Asian Financial Crisis of 1997-98, but household debt has been concurrently on the rise. From 72.6% of GDP in 2005, household borrowing has increased to 80.5% as of 2012 – as corporate balance sheets mended, household balance sheets have deteriorated.

This trend has come from a confluence of global and domestic macroeconomic factors such as low-wage competition (e.g. from China), wages progressively delinking from productivity, falling real interest rates, banks shifting emphasis from corporate to household lending, rising property prices, and a higher cost of living. While much of this household debt has been used to acquire properties and financial assets which could presumably back the attendant liabilities in the event of a crisis, there is a worrying heterogeneity in the distribution and direction of borrowing.

Something like 80% of household borrowing is by households that earn higher than average incomes (greater than RM3,000 per month, or US$1,000), and 46.5% are to households earning above RM5,000 (US$1,600) per month. The leverage ratio of the latter is in the region of 2.3-3.3 times annual incomes, a relatively comfortable level. For households earning less than RM3,000 however, the leverage ratio ranges from 4.4 to an astonishingly high 9.6 times annual income.

More worrying still, the fastest growing component of low income household debt is in personal loans, which are increasingly provided through the non-bank sector. The numbers are frightening – loan approvals through non-banks rose 63.7% in 2012, and the average personal loan was for RM68,000 (US$22,300) with a duration of 20-25 years.

This source of loans unfortunately lies outside the ambit of central bank regulatory oversight, a deficiency that Bank Negara Malaysia hopes to plug with the Financial Services Act due to come into force by mid-year 2013. Linkages with the broader banking system are limited as few non-bank financial institutions participate in the interbank market or rely on wholesale funding. Many of these low-income borrowers are also civil servants with good job security, and loans are paid off at source via salary deduction. The risk of a systemic banking crisis is therefore unlikely and any financial system fallout seems containable.

Be that as it may, there lies the socio-economic impact of revenue-constrained households with overstretched budgets, implicitly backed by an already indebted government. There’s little room for error with households paying up to 60% of their disposable income on principal and interest payments on debt. Though the Malaysian financial system appears to be largely insulated from the risks building up from low-income household debt, the government is not.

This is a much harder problem to solve than the government’s explicit and direct debt burden. Whereas the government has some leeway in determining its own revenue streams via tax policy, households do not. Moreover, with sufficient political will the government can change its behaviour to impact its financial standing. But reducing household leverage by changing the behaviour and the financial incentives faced by thousands of households is a policy challenge orders of magnitude more difficult.

Tightening monetary policy and enacting macro-prudential rules on lending might reduce loan supply, but would also increase financial fragility through higher interest rates. Fiscal consolidation is certainly called for to increase fiscal space to deal with any potential household debt crisis, but that too carries the same attendant risks. There’s certainly the option of growing out of the problem, but that implies a change in household borrowing behaviour that doesn’t appear to be on the horizon. There appear no easy answers to this conundrum.

HishamH is an economist at a large fund management company in Malaysia. He writes a blog on the Malaysian economy at Economics Malaysia.